The brand new TokenInsight report includes discussions on DeFi market landscape, including secondary market performance, DeFi’s TVL, Overview of the Decentralized Exchanges, Analysis on Automated Market Makers (AMMs).

July 16, 2020 by Johnson Xu

Head of Research & Analytics, TokenInsight

COVID-19 and DeFi Overview

The first half of 2020 has been shattered by the global COVID-19 pandemic which turns into a significant economic shock that creates a ripple effect on a global level. Decentralized finance is an exciting aspect of the cryptocurrency industry where it continues its innovation and growth at a significant pace despite the global economic downturn.

The decentralized finance ecosystem saw accelerated growth in the second half of 2019 where we have covered the growth in our 2019 DeFi annual industry report, with leading projects such as MakerDao, Uniswap and Compound Finance taking out solid positions in the DeFi ecosystem.

The most depressing moment in the first half of 2020 was the date that global financial market turmoil also spread to the cryptocurrency industry, the Black Thursday on March 12, 2020, at that time the industry saw a market-wide panic and dried up market liquidity which resulting market-wide liquidation and opened the door for system-wide structural risks to be surfaced in the cryptocurrency market, particularly in the DeFi ecosystem.

DeFi Conference 2020 Delivers an All-Star Speaker Lineup

When many people in the industry wishfully think the industry would shine in a big-time during a global economic crisis just like the one we are experiencing right now. The Black Thursday market crash, unfortunately, proved to many people that the cryptocurrency financial market is interconnected with the traditional realm, creating a cascading effect, and impacting every single aspect of the cryptocurrency market.

We are still growing fast in this early ecosystem, and a robust, structured decentralized financial system is needed to deliver the next-generation financial system to the world. The Black Thursday event was an early stress test to the DeFi financial system, and the industry held it together and successfully passed the early stress test.

Global zero-bound interest rate is potentially re-directing the money flow from the traditional market to the DeFi ecosystem where the interest rate is significantly higher than the one in the traditional system, although attracts higher risks compared to the traditional regime.

The purpose of the Q2 2020 DeFi industry report is to shed some lights on this lightning fast-moving DeFi ecosystem, and as an organisation to Find, Create and Spread value in the blockchain space. The Q2 2020 DeFi industry report has been broken into multiple parts including trading (DEXs, Derivatives and Prediction Market), Issuance (Stablecoins, Lending, Non-Fungible Token), Asset Management, DeFi Infrastructure and Others, Investment and Ratings where we work with Fundamental Lab to deliver this part.

DeFi Overview by Numbers

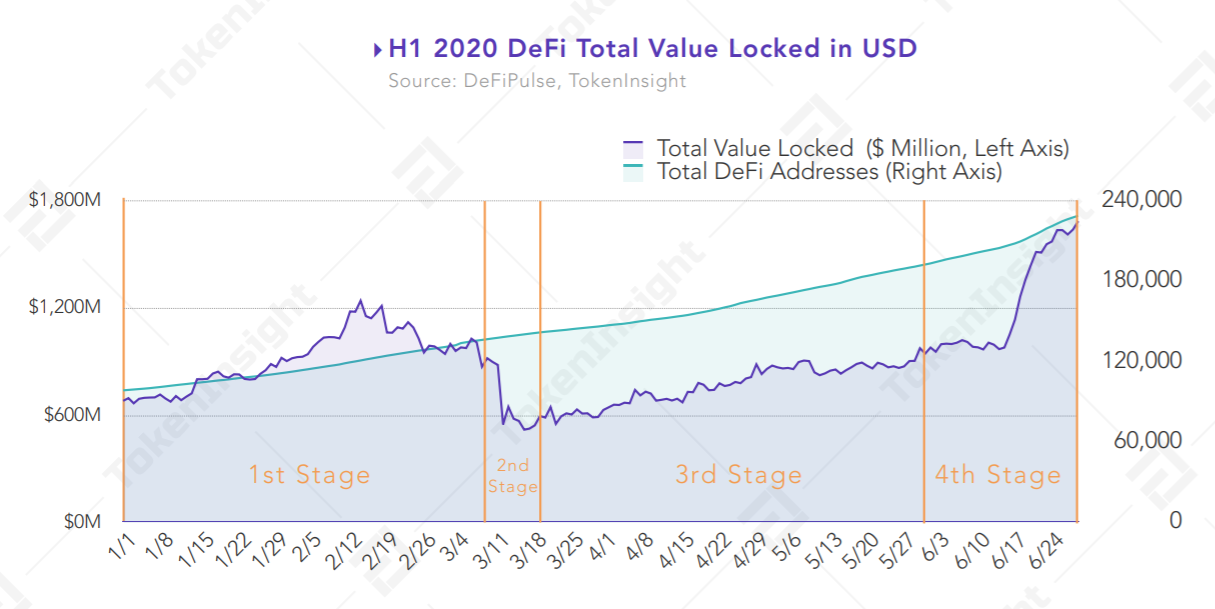

Total Value Locked in the DeFi ecosystem increased by $1 billion, an increase of 147% during H1 2020. Its growth rate is expected to remain steady upwards.

One of the most important metrics looking at the growth of DeFi is Total Value Locked in USD (TVL). The TVL has experienced dramatic increases from mid-June where it was hovering around 1 billion and jumped to more than 1.6 billion in just a matter of 2 weeks. The DeFi ecosystem experienced a significant downturn in mid-February from $1.2 billion in TVL to its recent lowest point of $500 million during the Black Thursday. Post-market crash, the TVL has been consistently increasing and shot up significantly due to the Compound governance token incentivised liquidity mining initiatives.

Throughout H1 2020, the amount of DeFi’s TVL went through 4 major stages:

- The growth phase from January to February 2020. TVL experienced a strong growth increased from $680 million at the beginning of the year and reached its local peak at $1.2 billion, and then fluctuated around $1 billion.

- Due to the impact of the global financial market downturn, the crypto Black Thursday market plunge resulting in the DeFi TVL fell off a cliff from $1 billion to its local low of $550 million.

- The recovery of the cryptocurrency market post-Black Thursday helped the DeFi TVL value to regain its position. The TVL slowly recovered from the Black Thursday low of $500 million to roughly $900 million.

- The explosive growth of the DeFi ecosystem due to the popularity of the incentivised liquidity mining (aka yield farming) in June 2020 combined with high lending interest rate attracted strong market interest in the industry and the TVL grew from $950 million to more than $1.68 billion, an increase of 77.6%

DeFi Sector Secondary Market Performance

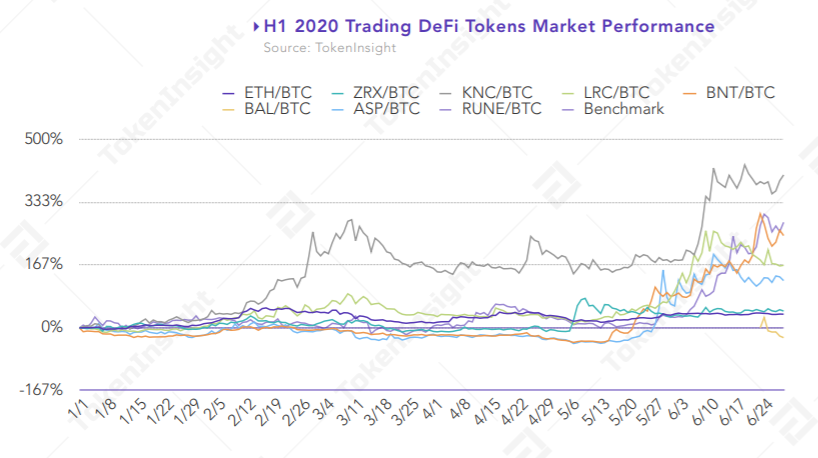

Overall, the holding period return for most of the DeFi tokens have outperformed Bitcoin and Ethereum in H1 2020.

Due to the industry hype around the DeFi concept in H1 2020, the majority if not all DeFi tokens delivered a strong return in the secondary market. Some DeFi tokens have outperformed the market (BTC & ETH) significantly from the beginning of the year, some surprisingly shot up quickly during June 2020 and delivered positive returns in the market.

Trading projects such as Kyber Network (KNC) delivered more than 4x return against BTC since the beginning of the year, ThorChain (RUNE) delivered more than 2x against BTC and Bancor Network (BNT) delivered more than 2x during H1 2020. Others such as 0x Project (ZRX), Loopring (LRC), Airswap (ASP) have all outperformed BTC and ETH. Balancer Protocol (BAL) launched its native token in mid-June 2020, although its secondary market performance is relatively weak, it delivered positive returns for the private sales investors who backed the project in the early days.

Lending sector also experienced strong growth in H1 2020, with Compound Finance (COMP) and Aave token (LEND) delivered 2x and 5x return against BTC throughout the 6 months. Compound Finance is one of the most anticipated lending projects in the DeFi space, its incentivised liquidity mining concept quickly gains market traction and aligned interest between lenders and borrowers, thus it quickly became one of the most trending projects in the industry. Its COMP tokens are being issued by the liquidity mining mechanism where lenders or borrowers deposit or borrow assets from the Compound Protocol in order to earn COMP token through the incentivised liquidity mining mechanism. The COMP token has experienced a wild fluctuation from its local bottom of $60 to more than $300 due to Coinbase listing and significant industry hype around DeFi projects. Others including MakerDAO (MKR), Kava (KAVA) have generally underperformed the ETH/BTC pair.

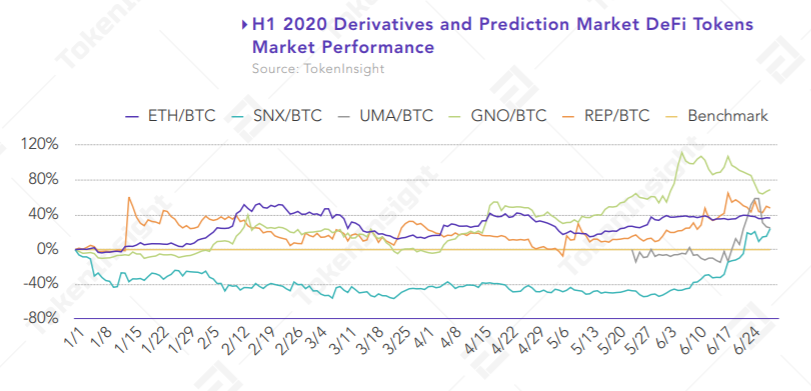

The derivatives and prediction market projects also saw a positive return but somewhat less than the return compared to lending and trading projects. Prediction market projects such as Gnosis (GNO) and Augur (REP) delivered the highest return in the sector with roughly 80% and 40% respectively.

Synthetix (SNX) as one of the most successful derivatives DeFi projects has experienced a relatively poor performance before June 2020 due to its strong secondary market growth in Q4 2019 where its token price experienced a significant price jump and subsequently experienced a mean reversion correction. However its token price took off again during June 2020 when the yield farming concept took off resulting in an industry hype around DeFi, and within a month delivered 100% return in the market.

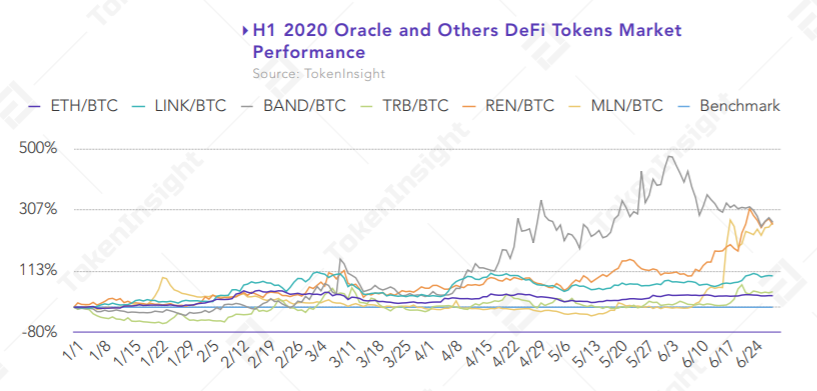

Oracle projects also performed positively compared to other DeFi projects in which Band Protocol (BAND) delivered nearly 500% return at its peak, other price oracle projects such as Chainlink (LINK) and Tellor (TRB) also saw moderate growth in the secondary market. Other projects such as Ren Protocol (REN) and Melon (MLN) performed reasonably well before June and experienced a jump in overall return during June 2020 alongside with other DeFi projects.

DEXs Overview

In H1 2020, trading volume on DEXs reached nearly $6 billion, an increase of 456% compared to H1 2019 and an increase of 141% compared to the 2019 yearly figure.

The trading volume for the year 2018 mainly came from Q2 2018 where the quarter’s trading volume accounted for nearly 49% of the total yearly trading volume in 2018. The 2019 yearly trading volume was almost the same compared to 2018. In 2020, the DEX sector as a whole entered a stage of rapid development, and its first-quarter trading volume ($2.3 billion) almost equates to the 2019 total yearly trading volume, with the second quarter volume jumped to a record high of $3.7 billion. TokenInsight Research expects that DEXs will maintain its development trend in H2 2020 in order to build a robust foundation for the future DeFi ecosystem.

TokenInsight conducted market share analysis on the 20 DEXs selected in H1 2020. Kyber Network’s market share saw a consistent downward trend in H1 2020. dYdX, Oasis and 0x Protocol’s market shares have grown slowly in the first 5 months of 2020 but have been squeezed out during June 2020 by the launch of Uniswap V2 protocol.

With the launch of Uniswap V2 protocol, it has successfully acquired more than 24% of the market share since June 2020. Combined with the market share of Uniswap V1, the Uniswap project became the biggest winner with a total DEX market share of 32% in June 2020, followed by Curve Finance where it’s market share jumped from 4% in May to 18% in June due to higher demands of stablecoins from the incentivised liquidity mining activities in the DeFi space.

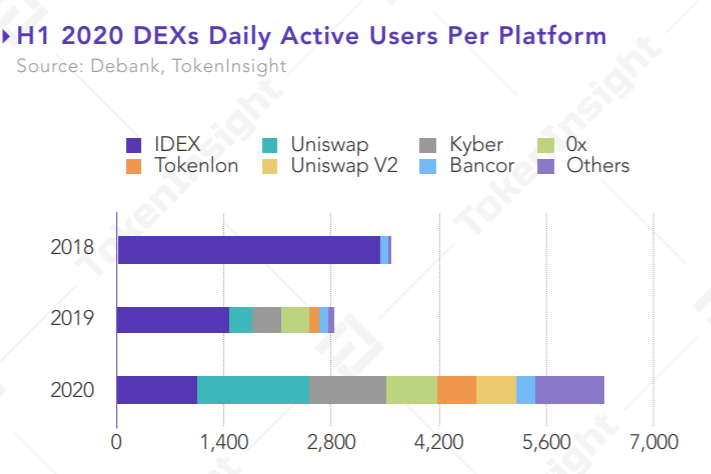

Extreme market conditions can temporarily stimulate users to enter the DEX market, but user stickiness remains limited. The number of active users in April 2020 fell back to the February level after the extreme market condition. After May 2020, the number of active users increased steadily, breaking the 10,000 mark.

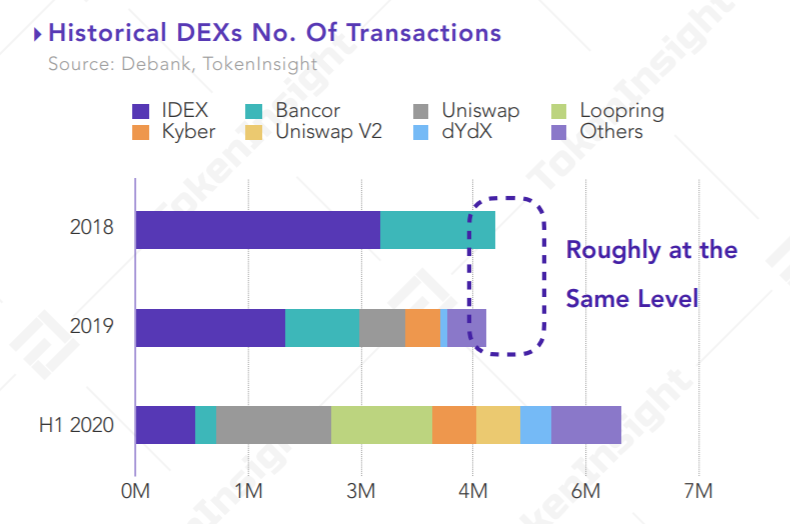

Compared with the previous two years, the total number of DEX tradings in H1 2020 has exceeded the figures in the previous two years. Uniswap and Loopring have acquired the top 2 positions on the number of transactions per DEX, and the No. of transactions for IDEX and Bancor V1 decreased sharply.

Projects Analysis and Comparison

In H1 2020, the total trading volume and the number of transactions in the DEX sector show that the top five DEX platforms account for more than 60% of the DEX market. Among them, Uniswap and Kyber Network occupy the first place in terms of the total trading volume and No. of the transaction respectively. The total trading volume and total transactions of these two DEXs account for more than 30% of the entire DEX market respectively.

The Loopring exchange was officially launched at the end of February 2020 and is the first DEX based on zkRollUp on the Ethereum mainnet. As shown in the figure above, in the second-month post-launch, the number of daily transactions exceeded 90,000, and the total number of transactions in H1 2020 have exceeded 1 million.

Although its number of transactions reached 21% of the total number of market transactions in the first half of the year, its transaction volume only accounted for 0.71%. TokenInsight Research believes that the number of transactions that can be achieved is mainly due to the ZK Rollup technology, based on the technology it requires a very low gas fee for each transaction. According to Dune Analytics data, the on-chain Gas fee only costs $0.0233 per transaction for Loopring DEX in H1 2020.

Unlike other DEXs, Curve Finance targets at stablecoins and wrapped assets liquidity provision. Based on the figure below, Curve Finance’s trading volume jumped during June 2020, where the incentivised liquidity mining concept gaining traction in the industry, directly driving the demands for stablecoins and wrapped assets trading.

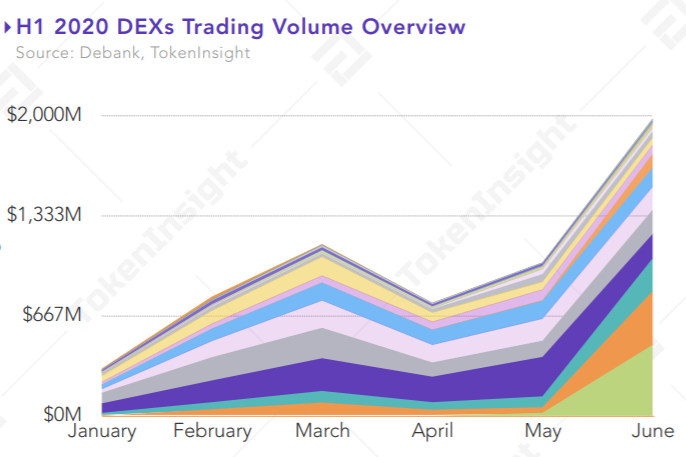

In June, the Automated Market Makers (AMMs) concept drove the market in the DEX sector. TokenInsight Research further compares the change in monthly trading volume between DEXs in the first half of 2020, as shown in the figure below. Among them, Curve and Uniswap V2 were the main contributing sources to the surge of DEX trading volume to the record high, in which the trading volume for Curve and Uniswap V2 accounted for 42% of the total market trading volume in that month.

Among the several DEXs with significant abnormal market performance in June, 1inch is a decentralized exchange mainly to help users choose the optimal path to achieve the lowest slippage when interacting with the DeFi ecosystem. In June, the trading volume accounted for nearly 50% of its trading volume in the first half of the year. TokenInsight Research believes that this is due to the fierce liquidity mining in June leading to strong demand for stablecoin in the market. Considering that 1inch have already integrated mStable and Curve, users can receive the best stablecoin conversion rate through 1inch.exchange.

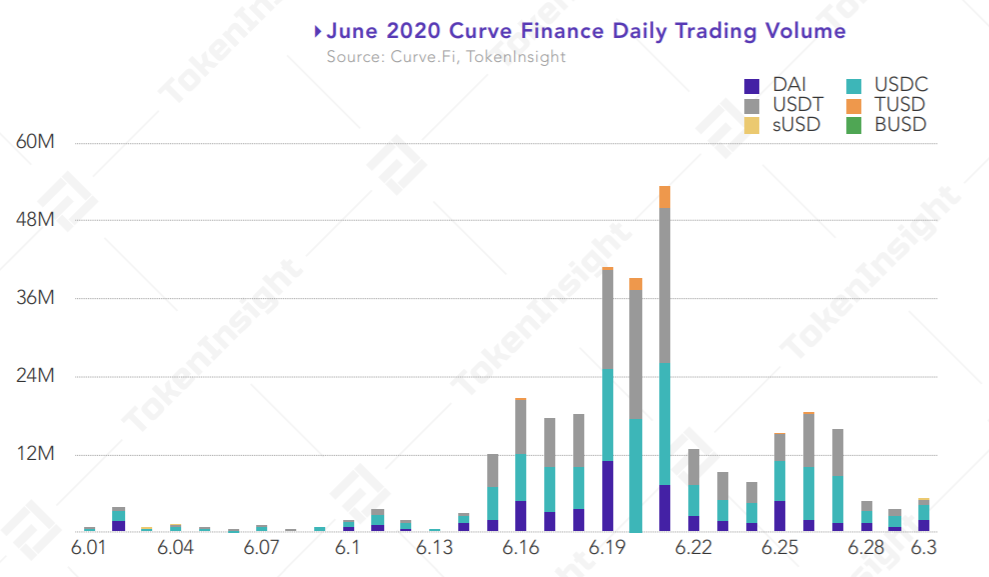

Curve Finance, which focuses on stablecoin and wrapped asset liquidity, saw a significant increase in trading volume in June 2020 due to the industry hype on liquidity mining which directly drives the demands of USDT or stablecoins in general in the beginning. On June 21 2020, the total trading volume on Curve Finance reached nearly $55 million while Uniswap V1 and V2 combined generated $22 million worth of trading volume. The following figure shows the daily trading volume of each stablecoins on Curve.

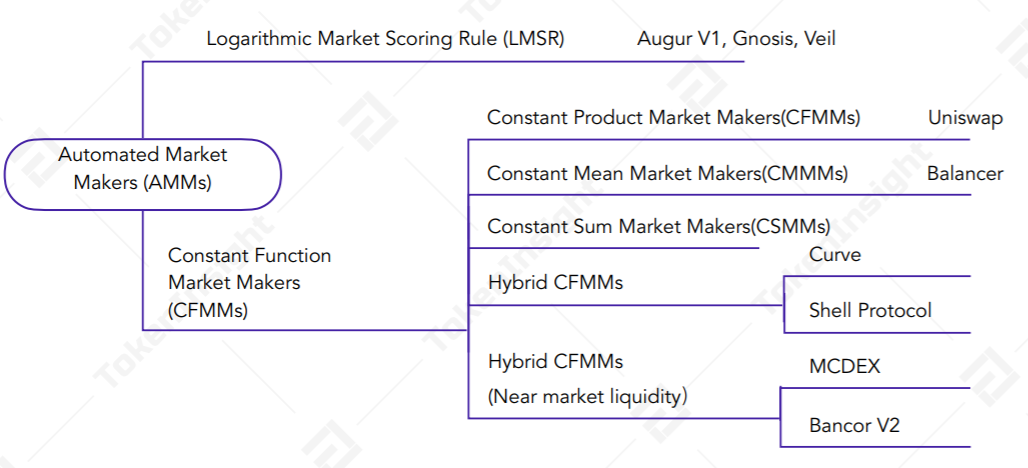

The DEX sector started to grow significantly in 2020, with a trading volume of roughly $6 billion in H1 2020. We have seen the competitive landscape changed significantly, and it is getting diversified by many innovative players entering the market. Based on the uncapped innovations brought by AMMs, TokenInsight Research classifies different AMMs into the following categorisations.

Final Thoughts

The development of the DEX sector experienced a pattern change in 2019 and then experienced significant growth in market activities in 2020. TokenInsight Research believes that the DEX sector is still in an immature state, and the increase in market trading activities in 2020 is coming from new DEX entrants. The Matthew effect (the stronger gets stronger, the weaker gets weaker) has not yet been demonstrated in the sector. We believe with the continuous development of the DEX sector, it will create ripple effects that could influence the DeFi space in all aspects, including the innovations of AMMs, improved governance mechanisms and project economic model.