Maelstrom’s chief investment officer warns that energy costs, a historic IPO glut, and political headwinds form a “toxic cocktail” for risk assets

Arthur Hayes, co-founder of BitMEX and chief investment officer of crypto-focused family office Maelstrom, has published a sweeping new essay arguing that the artificial intelligence investment supercycle is approaching a violent reckoning, and that Bitcoin, long expected to benefit from dollar liquidity expansion, will not be spared from the fallout.

In the piece, Hayes identifies “three darts” he believes will collectively puncture what he characterizes as an AI asset bubble inflated by roughly $1.5 trillion in debt issuance since late 2022.

Energy Costs: The Margin Killer

Hayes’s first concern is rising energy prices. AI data centers are, at their core, machines that convert electricity into intelligence, and that electricity is supplied predominantly by natural gas on the margin. An escalating military confrontation between the United States and Iran, which Hayes refers to as the “war waltz,” has already begun suppressing oil and gas supply through the Strait of Hormuz. Hydrocarbon inventories, he notes, are at their lowest levels in recent history and declining.

Should energy prices spike materially, Hayes argues, the economics of AI model production deteriorate rapidly. Token generation costs rise, margins compress for companies like Google, Anthropic, and OpenAI, and usage growth decelerates. That, in turn, calls into question the justification for the extraordinary data center capital expenditure programs that have defined the past two years, triggering multiple compression across the entire AI equity complex.

The IPO Avalanche: More Supply Than the Market Can Absorb

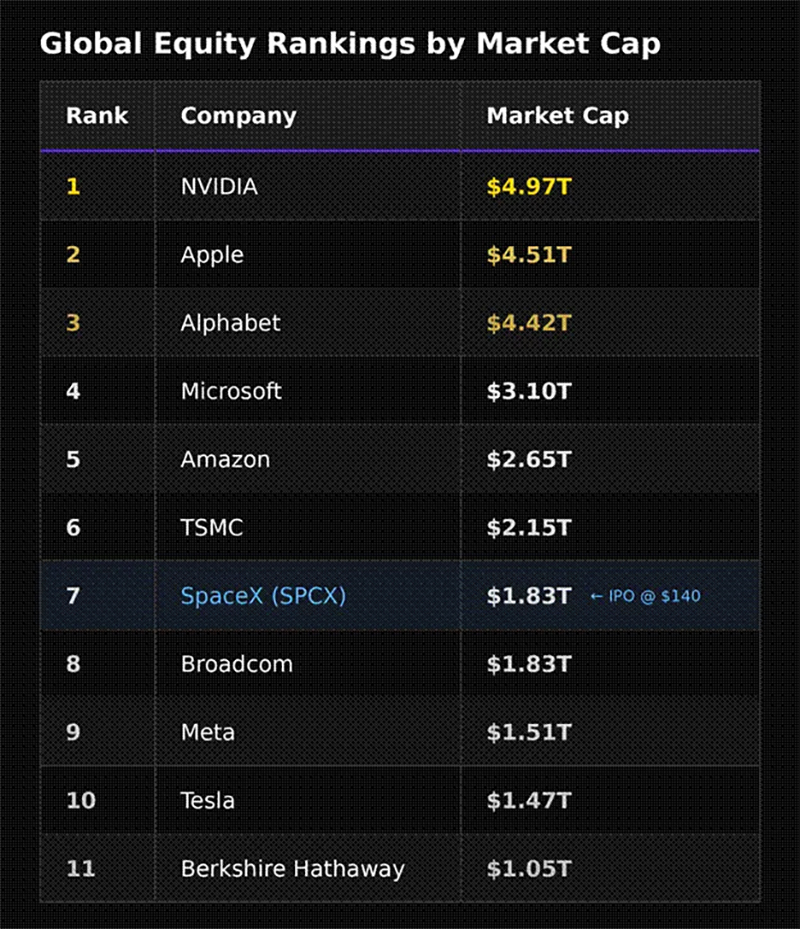

The second dart, Hayes contends, is the simultaneous public listing of SpaceX, Anthropic, and OpenAI—a capital raise he describes as exceeding, in aggregate, the total value of all dot-com era IPOs combined.

Hayes reserves particular scrutiny for SpaceX, whose S-1 filing he says implies a valuation of approximately 100 times sales, with only 4–5% of shares floated at launch. While he acknowledges the low float almost guarantees an initial pop, he argues the setup is structurally precarious: the company would instantly rank among the world’s seven largest by market capitalization, leaving almost no room for the continued appreciation markets expect from high-growth AI names.

“SpaceX will instantly be a $1.8 trillion company and the seventh largest globally by market cap,” stated Hayes. “To go up 50% would put it as the fifth largest company in the world just eking out Amazon, with nowhere near the earnings to justify membership in that rarified club.”

More damaging, he argues, is the vesting schedule. Between now and early September, SpaceX’s float is set to expand fivefold—a supply overhang that coincides almost precisely with the anticipated listings of both Anthropic and OpenAI, also at trillion-dollar valuations.

“When all three companies are simultaneously selling shares at insanely high multiples,” Hayes writes, “it guarantees market disappointment.”

According to him, “merely grinding higher is not enough” as the expectation is of an explosion higher in the stock price.

Trump’s Political Pivot: AI as Electoral Target

The third force Hayes identifies is political. If energy inflation persists and American consumers feel squeezed, he argues that the Trump administration will face mounting pressure to distance itself from the data center buildout and the tech establishment broadly. AI’s enormous appetite for power, land, and capital, as well as its association with concentrated Silicon Valley wealth, makes it a natural electoral target heading into the November midterms.

Hayes suggests that any sustained anti-AI rhetorical pivot from Washington would further erode investor confidence in the sector’s regulatory and fiscal outlook, adding political risk to an already fragile valuation environment.

On the Federal Reserve, Hayes adds a further complication: newly appointed chair Kevin Warsh is under pressure from the White House to cut rates, but market signals, including the 2-year Treasury yield trading more than 50 basis points above the effective fed funds rate, suggest the market believes rates should rise, not fall. A hawkish hold at the Fed’s June 16–17 meeting, Hayes argues, would function as tightening in all but name, compounding the pressure on risk assets.

“Both scenarios point to higher oil and natural gas prices three to six months out,” Hayes concludes, framing energy longs as the one asymmetric trade that pays across almost every scenario he can model. “Can the AI complex continue to rip at $150 oil? Doubtful.”

The Bitcoin Consequence

The essay’s broader thesis is that Bitcoin’s failure to rally in line with dollar M2 growth over the past year is not a flaw; in Hayes’s liquidity model it’s evidence that AI debt issuance absorbed essentially all newly created dollars. M2 expanded by roughly $1.5 trillion over the period; AI-related debt issuance totaled approximately the same figure.

The corollary, Hayes warns, is that an AI equity selloff will not simply leave Bitcoin unaffected. A credit contraction in AI lending, combined with margin calls on equity portfolios heavily weighted toward AI names, would suppress the marginal capital available for crypto entirely. Hayes confirmed he already liquidated positions in HYPE, NEAR, WLD, and ZEC in response, retaining only Bitcoin and Ether as core holdings.

“Ether is dead but functional. I have no immediate large capital demands that require liquidation of my Ether, so it shall stay unmolested,” writes Hayes.

Hayes’s longer-term view remains constructive though: he expects the eventual collapse of the AI bubble to precipitate a financial crisis significant enough to compel large-scale monetary stimulus, also known as “the Big Print,” at which point Bitcoin would stage a sharp recovery. But in the near term, he writes, capital preservation takes precedence over appreciation.

Hayes’s views represent his personal investment thesis and do not constitute financial advice.